Table of Contents

Executive Summary Key Points Introduction What ‘financialization’ is, and isn’t Class warfare by any other name Resource allocation and productivity In defense of profits The usual bogeymen Private Equity Hedge Funds High-Frequency Trading Banks Mergers & Acquisitions Dividends Stock buybacks Passive ownership/indexing Cures that are worse than the disease Monetary and fiscal policy getting a pass ConclusionExecutive Summary

Despite its ubiquitous use in modern America, the term ‘financialization’ is deeply misunderstood. Evidence shows the concept’s meaning often changes in different contexts. In some instances it serves as a relatively benign catch-all term for anything construed as a “greater role for the financial sector in the economy.” Others have described financialization as a “mismatch between the public interest and Wall Street interest.” In some instances, it is misunderstood as the simple pursuit of profit.

As the term ‘financialization’ has gotten more mileage in recent years, critics have seized on the ambiguity of the word to wage class warfare and attack capital markets, which are little understood. Among the most heavily criticized institutions and actions in the financial sector are the following: hedge funds, private equity, high-frequency trading, stock buybacks, dividends, and banks.

Key Points

This paper explores how the term ‘financialization’ has been employed—and explains why it should not be confused with mere financial sector activity—and demonstrates how its critics have done the following:

Inadequately defined the term Used a critique of the financial sector to disguise rank-class envy Failed to understand the nature of markets and the primacy of resource allocation Demonized instruments of financial markets that have been overwhelming positives for economic growth Proposed policy initiatives that would unilaterally do more harm than good Failed to see the most egregious actors in that which distresses them: excessive government debt and excessive monetary policyIntroduction

The term ‘financialization’ has received significant attention in recent years and is seeing far greater use in the vernacular of policymakers and thought leaders. The term is used in different ways by different parties, and a plethora of agendas exist behind these discussions. What’s clear is that there is growing interest in the role of financial markets in the broader economy.

While a treatment of financialization that embraces nuance is difficult in our time, no treatment will be coherent without nuance. The different uses, agendas, and contexts matter, and using vocabulary to poison a well is easy to do in this discussion, and also counterproductive. This essay explores the underlying concerns behind financialization, and seeks to more accurately describe what market forces do while addressing misconceptions about ‘financialization’ and free markets.

Conscious effort is required to avoid the laziness embedded in the label to paper over a class warfare argument. At the same time, advocates of robust capital markets concede that financial activities exist that offer limited productive value. In other words, it is entirely possible (and, indeed, will be the position of this paper) that what is often referred to as ‘financialization’ is no such thing at all, and is rather a misguided attack on all capital markets. And yet, it is also entirely possible (and the thesis of this essay) that a consortium of policies has facilitated what can be called financialization, and these policies should be rebuffed as contrary to the aim of a productive economy which facilitates maximum opportunity for flourishing.

In this nuance, we find the tragic irony of this contemporary debate. A growing movement, increasingly bipartisan, hostile to various activities in financial markets, has identified the wrong targets for critique. In so doing they not only have demonized healthy and vital components of an innovative economy but have missed the culprits who do warrant our attention. The reasons for this misidentification of cause and effect vary from a weak understanding of financial market reality to more severe ideologically driven errors. When the critics of financialization show a weak understanding of the problems they seek to solve, their proposed solution can only be flawed, incomplete, and misguided. Activities pejoratively referred to as financialization that are healthy and useful need to be defended. Likewise, activities, policies, and incentives that pollute the engines of a healthy economy need to be criticized. In short, a lot is on the line in this contemporary discussion.

The first section of this paper seeks to define what financialization is and what it is not. Upon establishment of a clear definition, analysis is needed to determine what is negative and what is positive. Once defined, an objective assessment of the causation of this phenomenon is in order.

After clarifying what financialization is, it will be useful to note the dangers of class warfare in the debate. This essay strives for an intellectually honest critique of any economic development or policy disposition that is weighing on the cultivation of prosperity. It does not seek to exploit or incite class envy. Nor does it seek to utilize demonization as a substitute for argument.

Critics of financialization, or at least those prone to using the term, have concerns about economic productivity and how resources are currently allocated. A basic refresher in how markets work and how resources are most efficiently allocated will be a useful foundation for this study.

In a similar vein to how class warfare underlies many misguided attacks on financial markets, a vigorous defense of profits is paramount to this discussion. Financial activity that hurts the common good is fair game for our scrutiny; an activity that is criticized merely because of its profitability is not. This essay will explore why corporate profits are vital in a prosperous society.

There exists a lengthy list of expected targets of criticism, even beyond the abstract and poorly defined “Wall Street.” Specific vehicles, institutions, and activities such as private equity, hedge funds, high-frequency trading, both commercial and investment banking, the payment of dividends, the buyback of corporate stock, and passive ownership of public equity all receive the ire of today’s market critics. In each case, their concerns ring hollow, incomplete, or woefully inaccurate.

An abundance of policy solutions now circulate seeking to remedy various conditions described herein. Eliminating bad solutions and embracing good solutions, all the while considering expected trade-offs, must be our aim. Unfortunately, many proposed remedies must be considered worse than the disease, and for this reason, also deserve our attention.

Likewise, it behooves us to consider the positive innovations in financial markets, fruits of a market economy and society ordered in liberty, that have demonstrably improved conditions for prosperity and flourishing. It does critics of finance no good to analyze that which is prima facie problematic without also looking at the clear positive results that robust financial markets have made possible.

And finally, we must look at that which is truly responsible for downward pressure on economic growth and productivity. Critics of financial markets so often reach over dollar bills to pick up pennies, concerning themselves with benign activities that present nothing more than a cosmetic concern, while ignoring the substantial and measurable negative impact of excessive government indebtedness, an obese regulatory state, an inefficient tax system, and most ignored of all, monetary policy that substantially misallocates resources.

Re-orienting our understanding of this subject will promote a cogent direction in economic policy and better move us towards the proper aim of financial markets—human flourishing.

What ‘financialization’ is, and isn’t

‘Financialization’ can mean different things in different contexts, but it generally carries negative overtones. The definition matters because, for some (including the author), there is a ‘financialization’ phenomenon that warrants significant criticism. But upon closer scrutiny, the actions most often described as ‘financialization’ warrant no such criticism. A coherent definition also allows for precision in what is being scrutinized and criticized, while failure to define the term properly risks generating an inadequate critique of what should be criticized, and a wrongheaded critique of that which should not.

There is an abstract but fair context in which financialization is a catch-all term for a “greater role for the financial sector in the economy.” At that level, it is a reasonably benign description and does not necessarily indicate any malignant effects on the economy as a whole or specific economic sectors. Here ‘financialization’ simply describes a scenario whereby capital markets activity becomes more prominent.

Other conceptions of financializations, however, are explicit in their condemnation of the manner in which financial markets re-allocate capital in ways that increase profits to owners of capital but without paying heed to what such critics’ conceptions of social justice or equality. An example of this is an American Affairs article that views financial actors as tools of “market worship” which, its author claims, undermines a just and responsible society.

A more particular definition of financialization might incorporate the influence or power of financial markets in overall economic administration. If we referred to the ‘technologization’ of society we would more likely be referring to a greater use of technology than increased power for technology elites, but it seems fair to allow for the inclusion of both—some increase of use and some increase of power.

Regardless, however, of what sector of the economy is having a new noun made out of its description, greater use of that sector is not self-evidently problematic. It may even be an obvious improvement (“medical sophistication”). Indeed, one could argue that influence or power is expected when greater utility is found in a particular segment of the economy. Whether it be consumer appetites or just general product novelty, the influence of various segments of the economy ebb and flow quite organically around their use, relevance, and capability. A generic increase in the use of financial services and accompanying influence lacks the specificity necessary to identify it as problematic.

As the term ‘financialization’ has gotten more mileage in recent years, those concerned with its allegedly malignant impact have taken advantage of the ambiguity, complexity, and mystery of capital markets (real or perceived) and present them as a malignant force. In this sense, class envy is a more likely description for much of what is described as financialization. It is therefore incumbent upon us to break down the ambiguity of where financial sector activity might be putting downward pressure on productivity, and where the term is being used only for its well-poisoning virtues.

Because financialization involves some basis for warranted criticism, mere financial sector activity is not the same as financialization. Likewise, increasing financial sector profits should not be considered the same as financialization. Critics are fair (prima facie) to suggest that if such profits come at the expense of other sectors, and at the price of total economic growth, then there may be a problem. However, the mere accumulation of financial sector profits is not financialization unless, in a zero-sum sense, such profits result from a decline in total profits and productivity. This will be a tough burden to overcome.

Is financialization the same thing as securitization, i.e., manufacturing financial products (securities) around other aspects of economic activity and streams of cash flow? Does the economy suffer when more components of economic life are securitized, meaning, capitalized, traded, valued, priced, and institutionally owned and monitored? Does securitization distract from organic economic activity, product innovation, and customer service? Or does it facilitate more of the above, mitigate risk, and enhance price discovery? Does securitization invite profits into the financial sector, while benefiting the public good by opening new markets for healthy activities (i.e. auto loans, inventory receivables, debtor financing, and more)? Is a critic of financialization willing to say that securitization enhances economic opportunity and activity, but still must be viewed skeptically because of the enhanced profits it produces for the financial sector?

Some have said that financialization produces a “mismatch between the public interest and Wall Street interest.” This may be getting closer, if we believe that scenarios exist where the production of goods and services that make people’s lives better are contrary to the wishes of Wall Street (i.e. our nation’s financial markets). Do those who invest, steward, trade, and custody capital do better when that capital is put to work for the public or against the public? It would be a high burden of proof to suggest that the financial sector at large (distinct from an individual actor) has interests disconnected from the broad economy.

The above listed distinctions and clarifications should make critics of Wall Street be more careful in framing their critiques of the financial sector. Confusing the financial services sector by giving the public exactly what it wants for working against public interest is a profound mistake. Close analysis of this dynamic reveals that what Wall Street is often being criticized for is not working against the public interest, but rather giving the public exactly what it wants too liberally. From subprime mortgages to exotic investments, many products and services may prove to be bad ideas, but they can hardly be called things that “Wall Street” distributed to “Main Street” against the latter’s will.

Nor should financialization’s problems be confused with the mere pursuit of profit. To the extent that critics of the profit motive exist, their philosophical objections are hardly limited to the financial sector. The productive pursuit of profits in a market economy is a good thing, and this judgment does not exclude the financial sector. The profit motive is not a problem in ‘financialized’ or in ‘non-financialized’ enterprises. Economic activity intermediated by financial instruments does not suddenly take on a different character. Rather, the problem is where more productive activities are substituted for less productive activities. If the production of goods and services towards the meeting of human needs is replaced by non-productive ‘financializing’, a problem exists that requires attention.

As we shall see, such ‘financialization’ does, indeed, exist. However, the culprits behind such are never the ones targeted by financialization’s loudest critics[1].

Class warfare by any other name

Associating Wall Street with greed and callous disregard for the public is not new. While Hollywood portrayals of Wall Street in the 1980s and 1990s focused more on hedonism and a general profligate culture, there has been a multi-decade distrust of “money changers” and various representatives of the financial markets of America. “Wall Street” has the disadvantage of being nebulous. It has not been known in a geographical context for a century, and its linguistic shorthand for capital markets is ill-defined and understood. What it is, though, is an easy target of the envious. It suffers from the lethal combination of being affiliated with riches and success, while at the same time lacking a clear definition. This tandem allows for an all-out class warfare on the very concept of Wall Street without any need for nuance or specificity.

Greed, arrogance, corruption, and disregard for the common good ought to be repudiated regardless of the industry in which they occur. These character components are common traits in fallen mankind, not unique to the financial sector. The particular disdain felt for Wall Street is really class envy that receives intellectual and moral cover from the widespread impoverished understanding of what our financial markets and the actors within them do.

We thus need a sober separation of the envy of wealth and success from a granular understanding of the work being done in any sector of the economy. A middle-class worker may believe a Hollywood A-list actor is grotesquely overpaid, or they may be jealous of the generous compensation that such an elite group of professionals enjoys, but demonizingall “acting” or “entertaining” makes no sense. Reasonable people can hold different subjective opinions about the talent of a given celebrity, but analyzing their theatrical or cinematic skills is hardly enhanced when buried underneath an intense jealousy of their compensation.

The same dynamics unleashed by envy and lack of knowledge applies to Wall Street and particularly the scrutiny of financialization’s role in driving or hindering economic productivity. That such a dynamic is common should not allow it to stand. Our economy either has a problem with financial sector activity in itself hindering productivity, or it doesn’t. We either need policy reforms to limit the use, power, and influence of financial markets, or we do not. The reality of this discussion is that those components of the modern economy that have most distorted and hindered economic growth are not as easily demonized as Wall Street, because bad policy, bad ideas, and the folly of central planning do not fall into a class envy narrative. A vital ingredient in our task is correctly identifying that class warfare is part of the ‘financialization’ critique.

Resource allocation and productivity

Getting to the core of this issue becomes possible once we accept that financialization, properly understood, is the substitution of productive activity with non-productive activity.. Financial markets involve the intermediation of capital in facilitating transactions, but they do much more. When one speaks of financial markets taking from another part of the market, what does that mean? How can we identify when this is occurring? What should we do about it?

Much of the problem comes down to not knowing what a market is. If markets were created by the state, or imposed by a third party, one could argue that the financial sector is negatively impacting markets. But a market is not imposed or created by the state or any other disinterested third party. A market is two people transacting. Embedded in market transactions are all sorts of realities about the human person. Humans make choice and act individually. They have subjective tastes and preferences, have reason, are fallible, have a high regard for self-preservation, and tend to pursue what they regard as their self-interest.

Given that humans are also social beings, most market activities also involve some degree of social cooperation. Our transactions with one another often take place in the context of a community. Our transactions often involve access to goods and services for entire communities. Steve Jobs did not make the iPhone for his childhood friend; he made it to scale distribution globally. Some products are purposely more limited in scope and appeal. The complexity and inter-connectedness of markets cause us to forget that markets are actions of mutual self-interest between free people.

When we hold to the fundamental basics of the market we are in a better place to consider where a financial sector may enhance the facilitation of our market objectives. Likewise, when we forget what a market is, we are more likely to be tempted by the allure of third-party actors to intervene, oversee, regulate, plan, and control the economic affairs of mankind. We forget that a market is grounded fundamentally on human actions at our peril.

In the context of free men and free women making a market together, negotiating the terms of trade, commerce, use of labor, and other conditions of economic activity, we can see both individually and cooperatively where financial markets can be a powerful tool of facilitation. Currency facilitates divisibility in exchange at the simplest and historically earliest of levels. Trading a herd of cattle for water presented challenges; trading with a currency to allow for settling accounts without impossible barter exchange values changed the world. Currency rationalizes exchange and facilitates more of it.

But it still must be said: the currency is not the end, but the means to the end. The financial instrument that facilitates the accumulation of water or cattle of whatever the goods or services may be is a mere tool. The resources being allocated, traded, pursued, exchanged, and acquired—enhances productivity and quality of life—are separate from the financial instrumentation. This intermediary functionality of money is a feature, not a bug. At the most basic of levels, it was the initial function of financial markets to drive resource allocation and free exchange.

It would be disingenuous to assert that all we mean, today, by financial markets is its intermediary function in exchange. Currency remains a vital part of economic activity and for much of the same reasons it was thousands of years ago. While the discussion of the financial sector facilitation of resource allocation begins with currency and it evolves, the fundamental function does not. When capital is made available for projects, the goods and services underlying the capital are still paramount. The use of debt or equity to entice support of a project invites a risk-reward trade-off, and creates a new “market,” but it does so towards the aim of an underlying market. Will customers like this product, or not? Will this entrepreneur execute? Is this cost of capital appropriate for this endeavor? Financial markets represent the pursuit of a return on capital, and yet, the return that capital rationally pursues comes from an underlying good or service.

Forgetting these points leads to economically ignorant conversations where you hear critics of financial markets suggest that we must stop talking about “cash flows” and “financial engineering,” and start focusing more on productive activity, customer satisfaction, and innovation. Where are “cash flows” from, if not the sales of goods and services? When financial activity is considered in the prospects of a business, or even for macroeconomic impact, it is all in the context of a “means to an end” – the instrumentation of finance to generate wealth-building activities. Financial resources (debt capital, equity capital, deposit funds, working capital, etc.) are evolved tools for driving resource allocation.

Our capital markets have matured and fostered innovation because, like our culture, they embrace and help us calibrate risk-taking. Devoting a significant amount of financial resources to a risk-taking enterprise is inappropriate for a person of limited means with certain obligations and monthly cash flow needs, lacking the capital to absorb losses. But the great projects that enhance our quality of life represent the risk of failure. Bank depositor money has only a limited capacity for loss absorption; a widow’s retirement savings might have no capacity for loss absorption; but money pooled and targeted for equity investment contains the risk-reward character suitable for investment. That our financial markets have developed, further, into more complex structures for both debt and equity, as well as various securitized options, does not alter this basic fact: Money is a mere instrument in allocating resources.

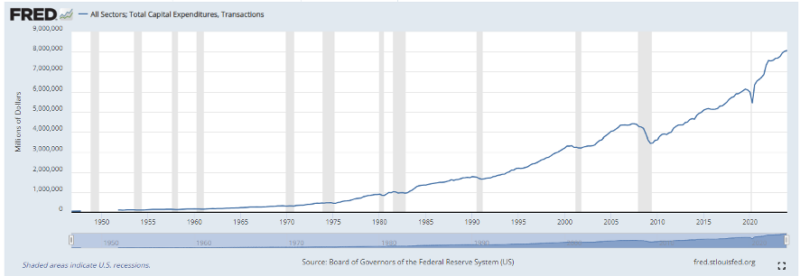

Have financial markets in the economy over the last five decades put downward pressure on capital expenditures, as we are often told? Quite the contrary, the empirical support is overwhelming that the evolution of capital markets enhanced capital expenditures over the last fifty years. The trendline was broken after the global financial crisis, but the upward trajectory of capital expenditures is indisputable.

Likewise with “non-residential fixed investment,” the so-called business investment component of how Gross Domestic Product (GDP) is measured, we see a steady increase in tandem with financial markets evolution. A post-crisis interruption of trendline growth will be better explained shortly, but fundamentally business investment has stayed robust as financial markets have innovated, grown, and evolved.

Perhaps an increased role of financial markets in the economy has not hurt capital expenditures or investment into new goods and services (i.e. R&D, factories, inventories, machinery, etc.), but has siphoned off profits from other sectors. Those making that specious claim carry the burden of proving it, but the empirical evidence is not up for debate. As the financial sector has become a modestly higher percentage of GDP, total national income has risen, making obsolete the fact that the financial sector’s portion of that income has risen, too.

The claim that profits from trade and production have been replaced with profits from financial activity is incoherent at best and patently false at worst. Profits inside the financial sector are tangential to the underlying activity of resource allocation. The financial sector is certainly capable of incorrectly allocating resources. Inherent to risk capital is the possibility of loss. Do financial markets allocate capital, subject to the trade-offs of risk and reward, more resourcefully and efficiently thanthe alternatives?.

What are those alternatives? One option is significantly limited access to capital markets, thereby limiting the instruments available for economic output. Another option is to meet capital needs with an expanded role for the state instead of using private capital. Again, the contest is between robust financial markets, declining financial markets, and greater governmental allocation of resources. These are the options on the table, and this is so because of what a market is. Markets allocate resources based on the decisions of people operating in their self-interest. Condemning financial markets for easing the operation of natural processes hampers economic growth and invites crony corruption.

In defense of profits

The topic of corporate profits is integral to discussions of financialization. Financial markets critics worry that profits have become problematic, and that ‘financialization’ is to blame. For our purposes, it is reasonable to ask if we are concerned with how profits are generated, or if we are concerned with what is being done with profits.

Many critics of financial markets claim that its profits are not connected to social productivity. This implies the existence of “socially unproductive” profits. Support for this view seems reasonable if we are talking about the profitability of certain unwholesome activities—strip clubs, online pornography, so much of the mindlessness of a gaming technology culture, etc.

But is the sentiment of “socially unproductive profits” putting a burden on profit makers and profit-seekers that is unfair? The general objective of meeting the needs of humanity through a profitable delivery of goods and services is unobjectionable. Profits become problematic when they are ill-gotten (fraud, theft, corruption), and yes, many would concede that profits from legal but also immoral activities warrant discussion. Yet the burden of creating fruitful and uplifting profit-creating activities belongs to the people in the market place and the associations and communities that constitute civil society – not the state. When undesirable activities occur, it is not the profit pursuit behind the activity that is the problem, but rather the problem itself. The last concern we should have with hired hitmen is their financial aspiration!

Concerns about “socially unproductive profits” is a category error that lacks a limiting principle. The creation of “socially productive” profits by disinterested third parties via intervention, cronyism, or some other form of central planning has to be read in the context of its trade-offs. The unintended consequences unleashed in this vision for society are catastrophic. It is not the burden of financial markets to resolve the tension that can exist between worthy social aims and profit-seeking activities. It is also untrue that financial markets exacerbate this tension. Because markets reflect the values, aims, interests, and intentions of free human beings, the financial resources behind these market-making endeavors will reflect the values of the people engaged in them. Demonizing the profit motive per se misidentifies the appropriate solution of moral formation and strong mediating institutions.

The financialization critique of profits is built on class envy and economic ignorance (not how profits are created, but what is being done with them). Robust financial markets allow for optionality that supports flexibility, choice, and future decision-making (for example, dividends, stock buybacks, and investing in corporate growth). Risk-taking owners receiving profits incentivizes future investment, promotes facilitates cash flow needs for investors, and enables consumption that satisfies other producers, and makes possible charitable bequests and other activities. Nothing in the prior sentence is possible without presupposing the existence of a profit. Optionality in what to do with profits is vital. The assumption that only the reinvestment of profits into more hiring, wage growth, further inventories, or other forms of business investment are appropriate is short-sighted, arrogant, and lacks factual evidence. Yes, some reinvestment of profits is generally warranted for the sustainability of a business. Many more mature companies reach a free cash flow generation that does not require additional capital reinvestment, but many do. Decisions around profit allocation are impacted by competitive pressures, company culture, investor desires, and other complexities.

What is not complex is that profits are the sine qua non of the entire discussion. Financial markets are a tool in generating profits whose very distribution is the subject of this discussion, and financial markets provide greater possibilities for how those profits are distributed. Profits themselves are not problematic, and in no way do financial markets “financialize” what is done with those profits. Optionality should be heralded, not condemned.

The usual bogeymen

At the heart of the modern crusade against financial markets are objects of ire: the institutions, innovations, and categories that become convenient targets for those who lament the role of the financial sector in the economy. As previously noted, these complaints are often reducible to rank class warfare. However, accepting the concerns at face value allows us to analyze many financial market innovations. This assessment should result in gratitude for capital markets, not condemnation. The following list is just an overview.

Private Equity

Perhaps no component of financial markets has become more caricatured and demonized than what is known as “private equity.” The words carry more connotation than just “equity ownership of companies that are not publicly traded.” The private equity industry is large, powerful, and dynamic, and has become a vital part of the American economy. To critics, this is something to bemoan. An objective analysis comes to a very different conclusion.

At its core, private equity represents professional asset managers serving as general partners, putting up some equity capital themselves (in amounts that can be majority ownership or often very limited), raising further equity capital from professional investors as limited partners, and taking ownership positions in companies. While the ownership is usually a majority position, it is almost always intended to be temporary (assume 5-7 years as a median hold period), and is very often financed with debt capital on top of the equity the general and limited partners put in.

The targets being acquired may be distressed companies whereby some enterprises have suffered deterioration and distress, and the hope is that new capital, management, and strategy may right the ship. But often the targets are highly successful companies that have achieved a certain growth rate and strong brand, but require additional growth capital to scale, more professional or seasoned management, or some synergistic advantage that a strategic partner can bring. And beyond the objective of “repaired distress,” and “growth and scale,” there is often an exit strategy for founders and early investors who can monetize what they have built by selling to new investors who could have any number of strategic or financial considerations in the acquisition (roll-ups, ability to introduce greater operational efficiency, etc.). Motives and objectives of buyers and sellers vary across private equity, and the industry’s growth and success have facilitated a highly specialized, niched, and diversified menu of private equity players.

There are various arguments made against the industry that are sometimes at odds with one another (they return too much capital to the owners compared to workers; but also, the returns are terrible and the industry is a sham). Opponents see private equity as either too risky, too opaque, too illiquid, too conflicted, or too unsuitable for the common good of society. Each concern deserves analysis.

First, the notion that private equity returns are terrible ought to be the greatest encouragement to the cottage industry of those concerned about private equity. If the returns on invested capital coming back to private equity investors were terrible, or even subpar, in any market known to mankind this industry would self-destruct over time. Sponsors would not be able to raise money. Limited partners would find other alternatives for the investment of their capital. Even acquisition targets (who generally carry some skin in the game) would seek better buyers out of their self-interest. Could some constituency of “sucker” leave some lights on longer than one might expect? Sure. But as a growing, thriving, popular institution in capital markets, private equity would evaporate if it were not generating returns that satisfied its investors. This strikes rational market students as obvious. Now, the range of return outcomes has historically been much wider for private equity managers than public equity managers, and the delta between top-performing managers and bottom-performing managers is much wider in private markets than in public markets. This is an advantage to the space, as skill is more predominantly highlighted, and noteworthy advantages are more statistically compelling, purging the space of poor performers and attracting more capital to diligent asset allocators. But no rational argument exists for why the largest, most sophisticated investors on the planet (institutional investors, pension funds, sovereign wealth, endowments, and foundations) would maintain exposure to private equity strategies with either inappropriate fees or inadequate results. If one believed that private equity was damaging to economic growth or the public good, poor investment results would be the ally of their cause.

Second, opacity and illiquidity are features, not bugs. Entrepreneurial endeavors are not straight lines. Businesses routinely face headwinds, cyclical challenges, unforeseen circumstances, and interruptions to strategy. Likewise, investors routinely face emotional ups and downs, sentiment shifts, and volatility of temperament. That a reliable capital base exists in private equity which prevents the latter (investor sentiment) from damaging the former (the realistic time frame needed for a business to succeed) is a huge advantage to the structure of private equity. Of course, some investors’ circumstances render illiquidity unsuitable for them. The solution is not to strip the illiquidity advantage and patient capital that it presents from private equity, but rather for free and responsible investors to exercise agency, and not invest where not suitable. Private equity provides a highly optimal match between the duration of capital and the underlying assets being invested.

Opacity is similarly beneficial. The better way to say this is that public markets suffer from the curse of transparency, meaning that competitors, the media, and all sorts of interested parties with any kind of agenda, are made privy to the deepest of details of the company’s financials, disclosures, and circumstances. For clarity, this is a trade-off that publicly traded companies accepted for other advantages to being public, but it is just that—a trade-off. All things being equal, there is no reason that a business would want the world to know its trade secrets, and financial dynamics in near real-time, let alone challenges and obstacles, especially not its competitors. The opacity of being private is not a negative; it is a tautology (when a company is private, it is private).

Finally, there is the concern that private equity is a negative force for workers. Specifically, the argument goes that private equity’s pursuit of operational efficiencies, the use of debt to fund the acquisition itself and subsequent growth, and the period promised to investors for an exit, all pit the interests of capital against the workers. There is, however, a fatal flaw in this argument, and that concerns the empirical data. Private equity-owned businesses employ 12 million people in the United States, a 34 percent increase from just five years ago. Eighty-six percent of private equity-owned businesses employ less than 500 people, and half of all companies with private equity sponsorship employ less than 50 people[2].

Interestingly, the National Bureau of Economic Research[3] found that where net job losses did occur (three percent after two years of a buyout and 6 percent after five years), it was predominantly in public-to-private buyouts and transactions involving the retail sector. Put differently, 20 percent or more job losses were highly likely had a public retail company failed, but a “take private” transaction minimized those losses. The same study found that private equity buyouts lead to the rapid creation of new job positions and “catalyze the creative destruction process as measured by both gross job flows and the purchase-and-sale of business establishments.” In other words, those who claim private equity leads to worse circumstances for laborers must establish that the jobs lost would not have been lost anyway.

That investors are not driven by the employee headcount is a given, similar to workers who are not driven by the ROI for investors. The argument for free enterprise is that there is a reasonable correlation of interest between all these parties and that the natural and organic tension between labor and capital is healthy and best managed by market forces. Demonizing this specific facet of financial markets (private equity) for possessing the same embedded tension as all market structures are selective, dishonest, and unintelligible.

Private equity defenders need not avoid the facts of failure. Private equity-backed businesses do sometimes (albeit rarely) fail. The reason is that businesses often do fail. The dynamic nature of market forces, changes, trends, consumer preferences, macroeconomic conditions, cost of capital, competitive forces, manager skill, and company strategy all lead to the very real possibility of failure, or what we learn as children to call “risk.” That private equity is not immune to risk is not a criticism. According to the Bureau of Labor Statistics, 20 percent of small businesses fail in the first year, 30 percent fail by the second year, and 50 percent by the fifth year[4]. Small business suffers a high rate of failure (and attendant job losses) because small business is hard. A more stringent regulation of small business or vilifying small business, though, would seem absurd to most reasonable people.

What about the argument that private equity uniquely increases risk by its use of debt? As we will see, there is a large actor in the American economy whose use of debt is threatening workers and the general welfare, but that actor is not the private equity industry. The capital structure of a business ought to be optimized to drive a healthy and efficient operation. Sub-optimal use of debt creates credit risk for lenders, and because debt is senior to equity in the capital structure, it threatens the entire solvency of the equity investors. In other words, ample incentives exist to prevent reckless debt use from doing damage. What is paramount, though, is that risk-takers suffer when there is a failure. Private equity works against the socialization of risk, but it doesn’t eliminate the existence of risk.

The private equity industry has added trillions of dollars to America’s GDP over the last four decades, employed tens of millions of people, added monetization and liquidity to founders and entrepreneurs, and created access to capital for talented operators who make the goods and services that enhance our quality of life. No part of this warrants skepticism or ire.

Hedge Funds

Similar criticisms exist for the hedge fund industry as private equity, in that many without skin in the game feel the fee structures and performance results are underwhelming. Again, it bears repeating that for the anti-hedge fund crowd, this outcome would be ideal. Indeed, over-priced and under-performing strategies have no chance of surviving over time. Some return-driven, self-interested investors must find something compelling within the hedge fund industry that keeps them returning for more.

That objective is a risk and reward exposure not correlated to the beta of traditional stock and bond markets. Idiosyncratic strategies may involve various arbitrage opportunities and the pursuit of mispriced securities and relationships, but the fee level and performance reflect an entirely different characteristic than that offered by broad stock and bond markets. This is not unknown to the investors of hedge funds but it is the entire point. Correlation is cheap (i.e. index funds), and non-correlation comes at a cost. Top-performing managers and strategies command a fee premium, and sub-par managers lose the Darwinian battle for assets. Market forces have a funny way of sorting this out, without the commentary of disinterested third-party critics.

Sebastian Mallaby’s masterful More Money than God: Hedge Funds and the Making of a New Elite[5] pointed out that hedge funds privatized gains and losses in the events of the 2008 global financial crisis, whereas the banking system allowed the socialization of losses even as gains had been privatized. Put differently, the banking system inherently poses systemic risks, risks that can be (and should be) mitigated and monitored. The hedge fund industry, though, represents an ecosystem of capital allocation, price discovery, information sharing, and profit-seeking, all with highly privatized risk and reward (as it should be).

Hedge fund criticism is always reducible to concerns the critics have with individual hedge fund operators (political, persona, etc.), or rank class warfare. That an alternative investment world exists where idiosyncratic trades can be executed, contrarian themes pursued, and various knobs of risk turned up and down (often with leverage and hedging) is an overwhelming positive to American enterprise.

High-Frequency Trading

High-frequency trading (so-called) has become a popular scapegoat for the anti-financial markets crowd. Advancements in digital technology have enabled complex algorithms to trade large blocks of shares of stock in nanoseconds. Those who have invested in this technology and infrastructure have bet on the ability of technology to identify opportunities and deliver value through speed and execution. Banks, insurance companies, and institutional investors can buy large blocks of stock quickly. Human decisions are disintermediated in favor of computers, and those utilizing high-frequency trading are accepting the trade-off that algorithms, speed, and execution will offer advantages over the cost of losing human interaction.

A trade-off is just that: a trade-off. The benefit of technological advancements in the trading of our capital markets has been unprecedented levels of speed and liquidity, which has meant dramatically lower costs of execution. Across our public stock and bond markets, trading costs are virtually zero, and bid-ask spreads are nil.

The advantages of high-frequency trading are obvious. But what about the disadvantages, and not merely the loss of human interaction the principal is now exposed to? Does this innovation pose the possibility of systemic risk, enhanced volatility, and system errors in our financial markets? Again, a better question would be: does high-frequency trading represent an exacerbation of those risks relative to what existed before it? Volatility, a mismatch of buyers and sellers, trading errors, and any number of market realities existed before high-frequency trading, and exist today (albeit with a bare minimum of instances of actual damage done). Market-making is a complicated business, and there is no question that high-frequency trading facilitates the making of a market (matching buyers and sellers, in this case at light speed). Opportunities for manipulation are highly regulated, and the net benefits from this innovation have spread to all market participants in greater liquidity, improved price discovery, and diminished trading costs.

Banks

From the days of the 1946 film It’s a Wonderful Life, the notion of a bank failure has been the subject of public fear and trepidation—and for good reason. Banks exist to hold customer deposits, facilitate customer payments from those deposits, and generate a profit by lending out those deposits at a positive net interest margin (i.e. the spread between interest paid to depositors and the interest collected on money lent out). Banks have largely been in the business of residential mortgage lending, but also handle 40 percent of commercial real estate lending in America[6]. Hundreds of billions of dollars of small business loans are also processed by commercial banks, funded by the capital base of the banks, which is largely depositor-driven.

That the banking business model effectively amounts to short-duration funding (i.e. bank deposits) being matched to long-duration loans (i.e. mortgages and business loans) is a theoretical flaw that is intended to be remedied by (a) Capital reserves, (b) Diversification, and (c) Quality underwriting. Liquidity issues can still surface when banking assets (the money they have lent out) prove to be longer duration than its liabilities (the money it owes its depositors back). Capital requirements mitigate if not fully eliminate, this risk, yet admittedly favor large banks to regional banks due to the disproportionate impact these requirements have.

Nevertheless, our financial markets, largely through trial and error and the lessons of experience, have increasingly presented the banking system as a store of value and a medium for payment processing, with engines of risk and opportunity increasingly coming from other aspects of financial markets. Banks still have a vital role to play in lending needs. Bank failures are increasingly rare, and competition has created ample optionality for the products and services banks offer (i.e. mortgages, credit cards, business loans, etc.).

Mergers & Acquisitions

Straight out of the class warfare playbook is the belief that investment bankers are money changers with no productive economic aim who are looking to squeeze money out of good and productive companies. Concerns about excess corporate deal activity are not limited to those who bemoan investment banking. Consider the words of one of the most highly regarded investment bankers of the last 75 years, Felix Rohatyn, atop his perch at Lazard in 1986:

In the field of takeovers and mergers, the sky is the limit. Not only in size, but in the types of large corporate transactions, we have often gone beyond the norms of rational economic behavior. The tactics used in corporate takeovers, both on offense and on defense, create massive transactions that greatly benefit lawyers, investment bankers, and arbitrageurs but often result in weaker companies and do not treat all shareholders equally and fairly … In the long run, we in the investment banking business cannot benefit from something that is harmful to our economic system.[7]

Like under-performing hedge funds or poor execution from high-frequency trading, the cure for bad Mergers and Acquisitions (M&A) is M&A. Markets will not support premiums irrationally paid for acquisitions (over time), and boards will not tolerate management eroding value through bad mergers (over time). Bad deals will happen, and good deals will happen, and short-sighted investment bankers will be incentivized to promote deals that do not represent good financial, strategic, or social sense. And yet, to not have access to robust merger and acquisition opportunities is to take away optionality in capital markets that are desperately needed. Competitive forces evolve over time in ways that can combine the embedded strengths of one company with the embedded strengths of another, creating value. The diversification of talent and subject matter expertise, properly channeled, is a huge benefit to our complex enterprise system and has allowed for the pairing of tremendous talent and corporate ecosystems that have created trillions of dollars of wealth. The simplicity of casting aspersions on all mergers and acquisitions because of the cases where some transactions proved ill-conceived is dangerous and harms economic opportunity. While it is incumbent on corporate management, company boards, and especially shareholders to resist unattractive M&A (that is, those with skin in the game), access to such innovation of capital markets is a vital part of our free enterprise system.

Dividends

Though not yet as demonized as stock buybacks, the return of corporate profits to minority owners via dividends is viewed as an example of ‘financialization’—as the favoring of owners of capital over the workers who help create corporate profits. Of course, these two things are not mutually exclusive. Owners are only paid dividends with after-tax profits, and profits are only realized after workers are paid. Dividends represent a substantial incentive to feed equity capital into businesses and therefore facilitate capital formation. The dividends then cycle through the hands of the risk-takers into their consumption desires or reinvestment aspirations. Any argument against dividends is an argument against profits, and an argument against profits is an argument against a market economy.

When we look at companies that failed after paying out dividends and buying back stock, the conclusion that it was a net loss to society requires an assumption of facts not supported by the evidence. That company not returning cash or buying back shares but continuing to invest in a failed business is what would have eradicated value. Cash to shareholders via share purchases or dividends allowed those owners to re-deploy capital in better businesses. And since dividends and share buybacks can only take place with after-tax profits, we are not talking about companies eroding the capital base of the company to pay them, but rather the allocation of profits after the fact.

Stock buybacks

Like dividends, share buybacks with after-tax corporate profits is a form of capital return to shareholders. As a professional dividend growth investor, I have ample reasons for believing dividend payments are a superior mechanism for the interests of shareholders. But the idea that share buybacks are inherently dangerous, short-sighted, or anti-worker, is demonstrably false. Once again, we are not talking about eroding the capital base of a company, but rather how to return capital to the owners of a business when that capital is enhanced by profit creation. Because many employees in public companies are paid via stock issuance (restricted shares, stock options, etc.), stock buybacks offset the theoretical expense that this form of executive compensation represents.

Examples exist of companies buying back stock at what is later revealed to be a high stock price, later running into cyclical challenges with the company operations, and having less cash to work through those times than they otherwise would have. All cases of a business challenge not perfectly predicted ahead of time are exposed to this risk. It does not address the underlying issue of share buybacks. If a company knew that it would later face an existential crisis and suffer a cash crunch, using the after-tax profits to pay down debt, pay bonuses to workers, or do anything other than increase reserves, would be unwise. This is not a unique burden for share buybacks, but rather a general challenge for businesses that are not guaranteed a perpetual path of easy profits.

Markets often provide incentives for corporate managers to use share buybacks more favorable to their compensation metrics than other forms of capital return. This is problematic. But it is a problem that must be addressed by those who bear risk, among managers, boards, and shareholders. The state has not proven itself a model capital allocator. For government to put its thumb on the scale of how companies allocate their capital is to invite distortion, corruption, and flawed information into economic calculation.

Passive ownership/indexing

Finally, there is the so-called passive ownership dilemma. An enormous increase in the popularity of low-cost index funds has led to a wide disintermediation of ownership across public equity markets. Passive stakes are voted on by non-beneficial owners like Blackrock and Vanguard. As the intermediaries who are legal owners, their agendas may conflict with the agendas of their customers. This issue can be solved in one of two ways: (1) Investors themselves will determine that their chosen intermediary is voting or operating in a way that does not serve their interests, and either choose a different intermediary or investment option; (2) Passive equity facilitators and managers will present innovations and options to solve for this tension.

The growth of passive/index strategy and the perceived power it gives these asset managers is a worthy conversation. It does not negate the substantial advantage of low-cost ownership and easy liquidity and access to public markets for investors, but it warrants attention and alteration to ensure that investors are receiving the best representation that achieves the highest returns on investment. Nevertheless, that attention and innovation are sure to be found in a combination of both #1 and #2 in the previous paragraph, and not by limiting the advent of passive equity ownership vehicles.

Cures that are worse than the disease

Opponents of financial sector growth have argued that the public interest calls for a variety of draconian measures to curtail freedom in capital markets. Introducing friction in financial sector activity by limiting its growth, protecting other economic actors, or generally reallocating capital in a way that central planners find more advantageous for the public good would accomplish this objective. All of these ideas carry unintended (or sometimes intended) consequences that would be counter-productive to the aim of economic growth.

A policy proposal to both suggest and critique is a special transaction tax on various stock and bond transactions in American public markets. Progressive politicians have taken advantage of the public popularity of this rhetoric (a “Wall Street tax”) to suggest that “free money” can be found by removing it from ‘financialization’ and into the coffers of the federal government for some spending initiative (Medicare for All, the Green New Deal, etc.). What is never understood, or otherwise is completely ignored, is that this money is not free. It comes out of financial transactions. This means that it becomes an additional cost to be borne by the private economy. The price may be paid by smaller investors who would incur greater trading costs, or it may be paid with less net money received in a particular transaction, leading to a less productive outcome over time for market actors rationally allocating resources. Regardless, it is not “free.”

Nor should we forget, it is not likely to work. Large institutions have resources outside of the United States for trading capital. Such a money grab would leave higher costs for smaller investors and sophisticated investors would pursue global options that avoid such a burden. Incentives matter, and the unintended consequences here would not curtail excesses in financial markets while raising money for other social aims. Rather, it would move money offshore, empower global competitors, and damage those who are not the target of the policy.

Some have suggested that making debt interest cost non-deductible would remove incentives to take on debt, thereby protecting workers in the case of companies exposed to excessive leverage. Of course, lowering the business income tax rates also better protects workers, and so removing a tool used to reduce that tax burden is simply the inverse when it comes to workers. Driving tax obligations higher does not protect workers. To the extent the policy succeeded in limiting debt, astute commentators might wonder what those costs would be. What is the debt being used for and what uses of capital would now be sacrificed if this policy suggestion prevailed? Will companies have less working capital, less liquidity, and be more susceptible to an equity sale (where job losses would be more likely, not less)? These expensive policy proposals have failed to count the costs, and in this case, the cost would be monumental. More than likely, the loss of deductibility of the debt would just be priced into the market rate of the loans, leaving less interest income for the lenders and banks, not a higher after-tax interest expense for the borrowers. In other words, it would be ineffective at best, and distortive at worst.

Various other proponents of de-financializing the economy suggest that increased tax rates would do this, including matching the tax rate on capital to the tax rate on income. The present tax policy is inefficient, but not for the reasons suggested by critics. Presently, a long-term capital gain of $100,000 creates a tax burden on the entire $100,000 in the tax year it was realized. However, a loss of $100,000 only allows for a $3,000 deduction in the year it was realized. This law was passed in 1977 but has not been updated for inflation. Furthermore, when a gain of $100,000 on capital is realized (real estate, stock, etc.), if their holding period was 10, 20, or 30 years, a significant part of the nominal gain was eroded by inflation, leaving the real gain to be a fraction of the total nominal gain. However, the capital gain tax is paid on the entire nominal gain.

Fundamentally, taxes on investment income are “double taxes”—as the money was already taxed when it was first earned (i.e. income), and now is facing additional tax when it is being invested (capital gains or dividends). But if that basic fact does not trouble the anti-finance constituency, the notion of matching income rates to investment tax rates can surely be done by lowering earned income tax rates. An increase in investment tax rates stifles capital formation, disincentivizes risk-taking, freezes capital in static projects, and impairs economic growth. If one wants to make a “fairness” argument for equal rates between tax on capital and labor, that fairness is already stretched in that the tax on capital represents a second tax on the same dollar. But if they persist in the fairness argument, lower ordinary income rates will likely be an agreeable solution for those wanting to protect capital formation.

From transaction taxes, to greater scrutiny of private equity, to changing the tax rules on debt or investment income, to various regulatory burdens on financial actors—no proposed solution from the anti-financial crowd serves workers or the cause of public interest. Rather, these and other proposed policy solutions invite hidden costs (and some that truly are not hidden), build state power, and damage broad prosperity.

Monetary and fiscal policy getting a pass

This concluding section can reasonably be called a tragedy. As was established in our early pursuit of a definition of ‘financialization,’ there is, indeed, an unattractive phenomenon that sub-optimally allocates resources. This ‘financialization,’ however, is not a by-product of more profitable investment banks, larger private equity managers, or increased technological capacity in capital trading. This ‘financialization’ where less productive activities take precedence over more productive ones is not created by Wall Street. Rather, the culprits are the very forces that the anti-finance critics are so often looking to play savior: the governmental tools of fiscal and monetary policy. In other words, the regulatory state, Congress, and the Federal Reserve are actors involved in this discussion, but not as fixers. The modern critics of finance have failed to identify the root causes of ‘financialization’ and in so doing have not only enabled the damage to continue but have invited them to do far greater damage, still.

No single factor has put greater downward pressure on economic growth than the explosion of government indebtedness, particularly, the ratio of that debt to the overall economy.

Common ground exists with those worried about diminished economic productivity and what that means to workers, and indeed, all economic actors. That common ground has not parlayed into shared despair over the growth of government spending, the growth of government debt, and the crowding out of the private sector both represent.

Furthermore, post-financial crisis monetary policy has been a series of gigantic monetary experiments that have served to do the very thing that critics of financial sector activity profess opposition to. Defenders of interventionist monetary policy may claim that it served to stimulate the economy post-crisis and to reflate the corporate economy as the household sector de-leveraged in the aftermath of the housing bubble. Yet even the most zealous defenders of that trade-off could not argue that such a monetary framework came at no cost. That cost was a substantial increase in real financialization.

The fiscal components are easy to identify. Government debt represents dollars extracted from the private sector either in the present or future tenses. A Keynesian would argue that such debt when used for productive projects like the Hoover Dam adds to GDP (a positive multiplier). However, present debt explosions have not been to build a Hoover Dam. Post-crisis spending exploded above the trendline, well before the 2020 COVID pandemic. The spending response to COVID created a huge outlay of expense, unfortunately as the pandemic subsided and all pandemic-related expenditures were completed, expenditures resumed far above the trendline, and far above the level of economic growth.

The federal government is doing what Goldman Sachs, Blackstone, and JP Morgan have never done—removing resources from the productive portion of the economy to the non-productive. It is outside the scope of this paper to evaluate what government spending projects ought to be. One can believe that current spending priorities are legitimate without believing they are productive. Some cost of government is necessary, and that funding will come from the private sector. However, when the cost of funding the government grows exponentially quicker than its revenue sources, and when the level of debt accumulates to the absolute levels it has, and with the annual debt funding costs it has, then declining productivity is the ultimate result.

Economic growth pulled into the present means less economic growth in the future. In the current debt predicament, this is not even economic growth pulled forward, but rather the accumulation of seemingly endless transfer payments. This extraction of wealth from the private sector to fund income replacement does not produce anything nor build anything. A real GDP growth rate that has declined from over +3% to below +2% measures the impact on economic output.

The monetary component of this strikes at the heart of resource allocation. If the Federal Reserve was tasked with holding interest rates at a natural rate, it would be at that level where economic activity would be most “natural”—where the interest rate was neither incentivizing nor disincentivizing economic activity. For 14 of the last 16 years, the Fed held the interest rate at or near zero percent, well below the natural rate in all but the most extreme crisis years out of 2008. That artificially low cost of capital extended the lifeline of many over-levered economic actors, and in the early years of post-crisis economic life likely facilitated some productive reflation. Yet over time, the perpetual zero-bound rate target encouraged economic actors to bypass the production of new goods and services for financial engineering. Incumbent assets in the economy—real estate or equity stock already in existence—could be bought and levered with little financial risk, with the low cost of leverage intensifying returns for these economic actors. Such activity was far more attractive than the creating new projects, sinking capital into new ideas, and innovating with one’s capital at the risk of loss. The zero-bound was a substitute for new goods and services, and it has taken a toll on productive economic investment.

Likewise, a prolonged unnaturally low rate facilitated ongoing resources into sub-optimal assets, keeping “zombie” companies alive where a natural cost of capital would have expedited their demise. While seemingly generous in its impact, the real cost of this process is in the resources that do not work their way to innovation, new growth, and new opportunities. Overly accommodative monetary policy extends the lifeline of those whose time has come and gone preventing fresh ideas from receiving the capital and human resources they need to breathe life into the economy. It fosters malinvestment, distorts economic calculation, and wreaks havoc on economic growth.

The twin towers of fiscal and monetary policy are powerful economic levers. On one hand, the fiscal tool crowds out the private sector and inhibits innovation by taking from the growth of the future to fund excessive spending today. On the other hand, the monetary tool uses the cost of capital to manipulate economic activity, ignoring the diminishing return and obvious distortions created by their efforts.

If one is looking for a malignant financialization, they have found it, and Wall Street is nowhere near the scene of the crime.

Conclusion

Critics of financialization have:

Ambiguously or inadequately defined the term, Used a critique of the financial sector to disguise class envy, Failed to understand the nature of markets and the primacy of resource allocation, Demonized instruments of financial markets that have been overwhelming positives for economic growth, Proposed policy initiatives that would unilaterally do more harm than good, and Worst of all, failed to see the most egregious actors in that which distresses them: Excessive government debt and excessive monetary policyAn optimal vision for the economy does not favor the financial sector over the “real economy,” nor does it pit the financial sector against the real economy. Rather, an optimal vision sees financial markets as capable instruments in advancing the economic good and public interest. A large public bureaucracy cannot improve the economic lot of workers, and diminished financial markets cannot optimally allocate resources to the real economy.

The need of the hour is better price discovery, starting with the price of money. The cost of capital as a tool of manipulation in the hands of our central bank has facilitated ‘financialization’ and hampered productive economic activity. The tools of modern finance can advance the cause of prosperity when we limit distortions in economic decision-making, maximize the availability of resources in the sector of the economy most equipped to utilize those resources productively, and remove impediments to growth.

Human beings are capable of great things. Advanced financial markets enhance those capabilities and build opportunities for the future.

[1] For an entire case study on poorly defined ‘financialization’ and ignoring data to allow a false narrative to stand, or twisting to data to create a false narrative, see https://americancompass.org/yes-financialization-is-real/, by Oren Cass.

[2] American Investment Council, Economic Contribution of the U.S. Private Equity Sector, Ernst & Young, May 2021.

[3] National Bureau of Economic Research, Working Paper 17399, Private Equity and Employment, Jan. 1, 2012.

[4] Bureau of Labor Statistics, Survival of Private Sector Establishments by Year, March 2023.

[5] More Money than God: Hedge Funds and the Making of a New Elite, Sebastian Mallaby, Penguin Press, June 2010.

[6] MacKay Shields Insights, Mark W. Kehoe, Banks and Commercial Real Estate, April 11, 2024.

[7] The New Crowd, Judith Ramsey Ehrlich, Harper Collins, January 1990.

Download the Paper

More Stories

The State of Competitive Federalism

The State of Competitive Federalism

The State of Competitive Federalism